Why Cathie Wood is Loading Up on These 2 Growth Stocks (And Should You?)

When Cathie Wood’s ARK Invest adds stocks to its portfolio, it tends to catch attention. Wood is not your typical Wall Street investor; her strategy is based on strong conviction, disruptive innovation, and long-term horizons. She is well-known for funding groundbreaking ideas in artificial intelligence (AI), genomics, robotics, energy storage, blockchain, and other "next-gen" technologies that many others regard as too risky or speculative.

On Sept. 10, Wood added Rubrik (RBRK) and Prime Medicine (PRME) to her portfolio. But Wood isn’t known to buy blindly. There are several compelling reasons why Rubrik and Prime Medicine piqued her interest. Let us see if these two growth stocks are worth the investment.

Why Rubrik Aligns With Cathie Wood’s Playbook

On Sept. 10, Wood’s ARK Next Generation Internet ETF (ARKW) bought 66,836 shares of Rubrik for $6.6 million, bringing the total investment in the company to $35 million. It comprises 1% of the overall portfolio.

Valued at $15.2 billion, Rubrik is a company specializing in data security, backup, recovery, and cloud-based protection of data, especially in an era where ransomware and data breaches are growing risks. RBRK stock has gained 17% year-to-date (YTD), compared to the overall market gain.

Rubrik may have attracted Wood's attention due to its rapid rise in subscription and recurring revenue. This is an important indicator for growth investors since it indicates predictability, durability, and scale. Rubrik’s recent second quarter highlighted its strength in the rapidly expanding cyber resilience market. In Q2, the company reported subscription annual recurring revenue (ARR) of over $1.25 billion, up 36% year-over-year, fueled by $71 million in net new subscription ARR. Within that, cloud ARR surged 57% to $1.1 billion, reflecting strong adoption of Rubrik Security Cloud.

Notably, overall revenue increased 51% to $310 million, with subscription revenue up 55%. As a rapidly growing cloud company, profitability remains a question mark. However, adjusted net loss narrowed to $0.03 compared to $0.40 in the year-ago quarter. Adjusted gross margin also improved to 82% from 77% a year earlier, fueled by lower hosting costs, operational efficiencies, and scale benefits.

Furthermore, free cash flow improved to $57.5 million from a negative $32 million last year. Rubrik's balance sheet, which includes $1.5 billion in cash and marketable securities and $1.1 billion in convertible debt, is well-positioned to sustain ongoing expansion initiatives.

Analysts predict Rubrik’s revenue to increase by 39.2% in 2025, followed by 25% growth in 2026. Wood's addition of Rubrik to the ARK Next Generation Internet ETF is not surprising given the company's improved fundamentals, increased margins, and positive free cash flow. Wood is probably betting that Rubrik's combination of growth, profitability improvements, and exposure to the cybersecurity megatrend will position it as one of the leading cloud security names in the coming years. For investors drawn to growth, innovation, and willing to stomach risk, Rubrik may be a growth name to watch very closely.

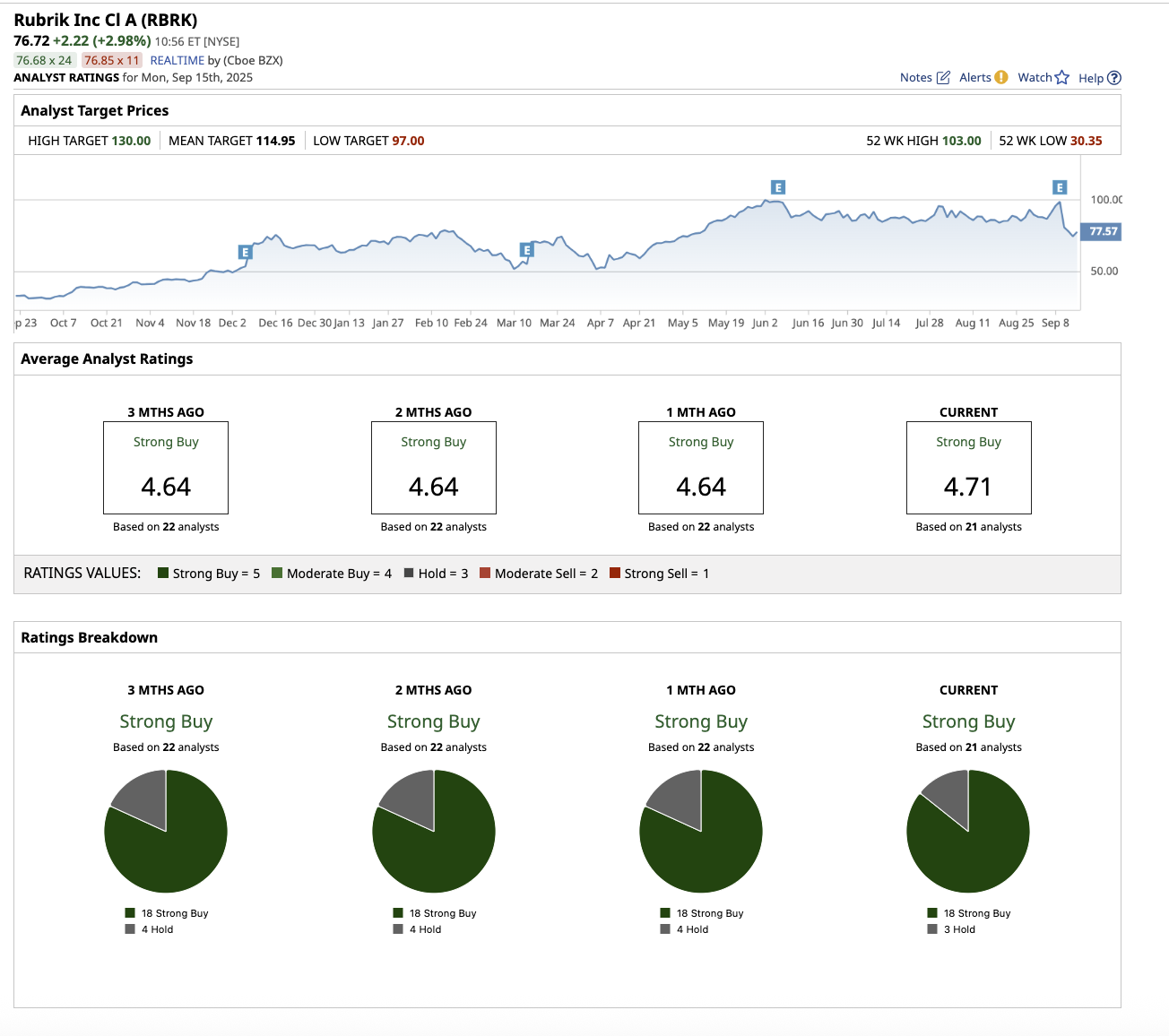

Overall, on Wall Street, Rubrik stock is a “Strong Buy.” Out of the 21 analysts that cover the stock, 18 rate it a “Strong Buy,” and three suggest a “Hold.” The average target price for Rubrik stock is $114.95, representing potential upside of 49.8% from its current levels. The high price estimate of $130 suggests RBRK stock can rally as much as 69.4% this year.

Why Prime Medicine Aligns With Cathie Wood’s Playbook

On Sept. 10, ARK’s Genomic Revolution ETF (ARKG) added 230,755 shares of Prime Medicine, worth over $950,710, increasing its total investment in the company to $19 million. It is the ETF's 19th largest holding, accounting for 1.9% of the whole portfolio.

Valued at $697.7 million, Prime Medicine is a biotechnology company developing gene-editing therapies using Prime Editing, its next-generation gene-editing technology. Its core focus areas are liver diseases, lung diseases, immune and cancer therapies, and rare diseases. PRME stock has soared 32.9% YTD, outperforming the broader market.

A noteworthy breakthrough in the second quarter was the announcement of positive Phase 1/2 data for chronic granulomatous disease (CGD). The findings from two patients offered the first clinical proof that Prime Editing can restore key immunological function in humans. These findings validate Prime Medicine’s platform, which is why Prime intends to work with the FDA to explore ways to make its CGD treatment available to patients sooner.

As a clinical-stage biotech, the company posted a net loss of $52.6 million in Q2. However, Prime Medicine held $115.4 million in cash and equivalents at the end of Q2, excluding the fresh capital from its August financing. Combined with support from the Cystic Fibrosis Foundation, the company has established a strong financial position that will allow it to continue its R&D work long into 2027.

Beyond its current pipeline, Prime Medicine focuses on the adaptability of its Prime Editing technology. The platform is intended to fix nearly all sorts of genetic mutations with precision, minimizing off-target edits and allowing for application across many tissues and disorders. The company has the opportunity to diversify into immunological disorders, cancers, infectious diseases, and even common diseases with genetic risk factors. Wood sees Prime as a high-risk, high-reward opportunity that might transform the future of genetic medicine.

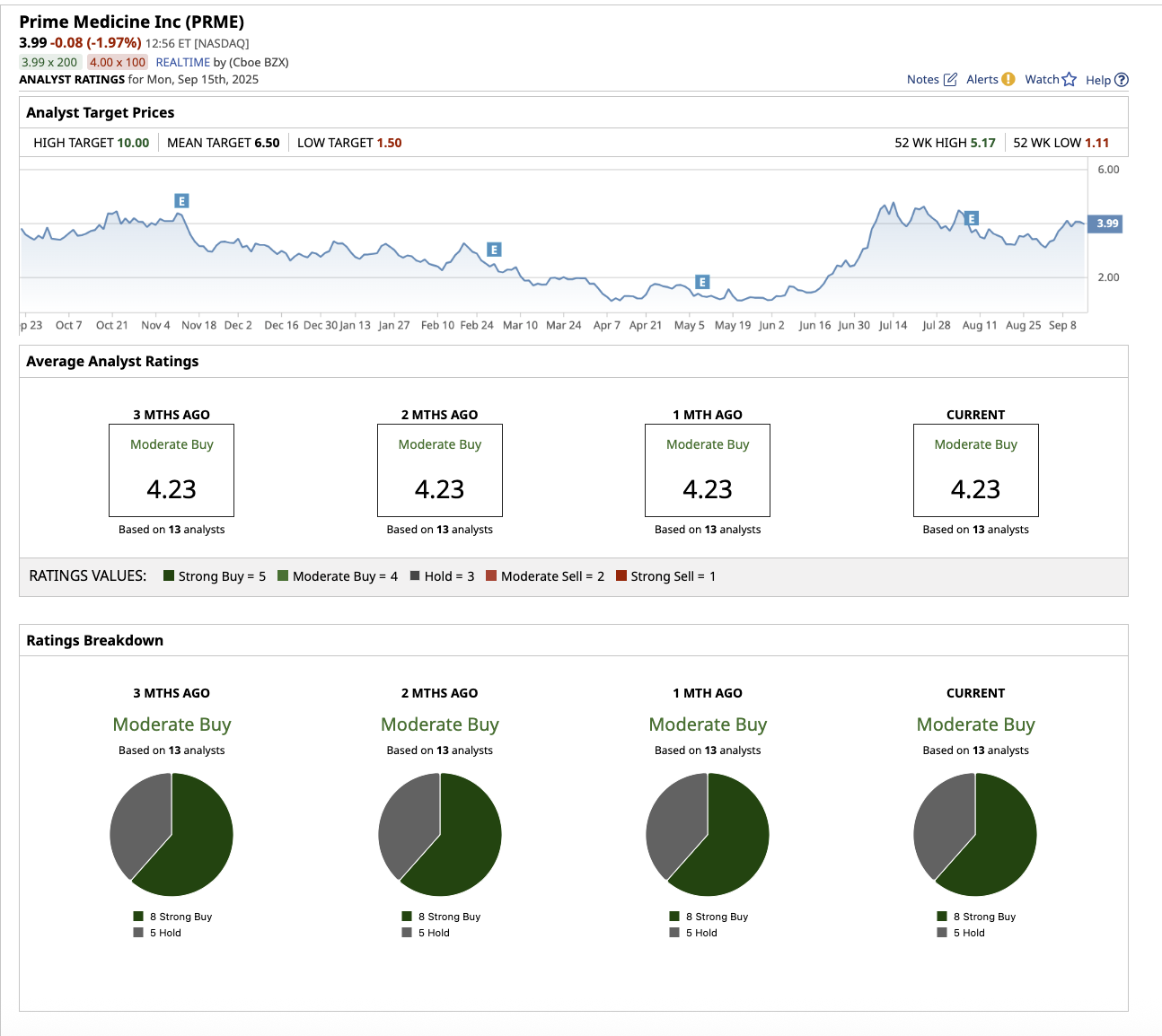

Overall, on Wall Street, PRME stock is a “Moderate Buy.” Out of the 13 analysts that cover the stock, eight rate it a “Strong Buy,” and five suggest a “Hold.” The average target price is $6.50, representing potential upside of 63% from its current levels. The high price estimate of $10 suggests the stock can rally as much as 150.6% this year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.